Critical illness insurance can be a vital part of your financial security plan if you’re diagnosed with a condition such as a heart attack, stroke or life-threatening cancer. If you are diagnosed with a covered critical condition and satisfy the survival period, the benefit you receive can help you deal with unexpected expenses, meaning you are less likely to dip into your existing savings to meet unexpected expenses.

But what if you don’t develop a critical illness?

Many critical illness insurance policies allow you to add an optional return of premium rider that rewards your continued good health. This return of premium rider could help you recoup some or all of the eligible premium paid if you never make a claim.

Here’s how it works.

Eligible premiums are returned if you don’t make a claim

If you remain healthy and have a return of premium rider, all or a portion of the eligible premium paid is returned.

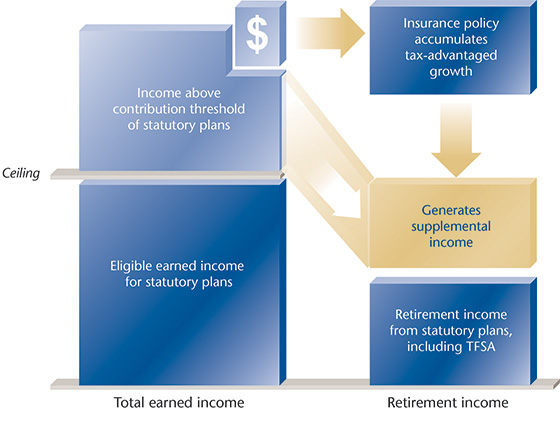

Returned premiums can be used to supplement retirement savings

If you don’t make a claim and you receive a return of premium benefit, the money you receive can be used to fund investment strategies as you near retirement. So, while the premiums are typically higher on a policy with a return of premium rider, you can invest the amount of premium returned under the rider.

Most people never prepare for a critical illness

Deciding to include critical illness insurance in your financial security plan is an important way you can reduce financial risk and help protect your savings. Adding a return-of-premium rider can help you continue to protect those savings and help fund your financial goals.

I can help you tailor your coverage by discussing the various return of premium options that may be available to you. Set up a meeting today to put plans in place to reduce your financial risk if you suffer a critical illness.

*The

The Canada Revenue Agency and Revenue Quebec have not provided a formal ruling confirming that policies which include return of premium benefits are accident and sickness insurance for income tax purposes. The tax treatment of optional return of premium benefits is subject to interpretation.